Entries from August 25, 2019 - August 31, 2019

UK data wrap: more recessionary indications

Simon Ward

Simon Ward

Post a Comment

Post a Comment

UK economic news remains consistent with a recession having started in Q2.

The CBI’s expected growth indicator – a GDP-weighted average of future output or sales responses from its monthly surveys of manufacturing, distribution and other service industries – is estimated to have plunged into contraction territory in August; the CBI will release the August result over the weekend – see first chart.

An early recession warning was a contraction of real M1 holdings of private non-financial corporations (PNFCs) in the six months to February, signalling likely business retrenchment. July monetary data released today show that the six-month change remained negative last month – second chart.

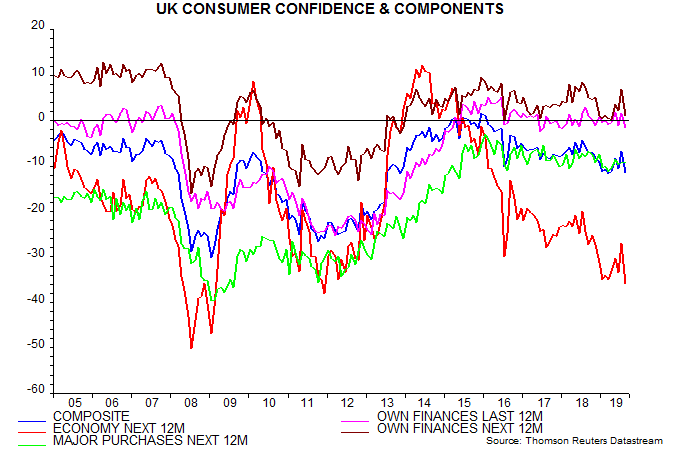

Household real M1 holdings are still growing but have slowed, with further weakness likely as a softer labour market curbs income growth. Households were markedly more pessimistic about recent and prospective trends in their finances in the August GfK / EU Commission consumer survey, contributing to a large drop in the composite confidence index – third chart.

Euroland money trends suggesting 2020 recovery

Euroland money measures grew strongly in July, more than compensating for softer June data and suggesting improving economic prospects.

Previous posts argued that economic momentum would bottom around Q3 and recover into 2020, based on a strong rise in six-month real narrow money growth between November 2018 and March 2019. The monetary pick-up stalled in Q2 but is now back on track, while the manufacturing PMI appears to be stabilising on schedule – see first chart.

Six-month growth of nominal narrow money rose to a 25-month high in July – second chart. The Q2 pull-back in real money expansion reflected a rise in six-month consumer price inflation but this is probably peaking.

Narrow money acceleration is being driven by plunging bond yields, which have moved to discount a major ECB easing package next month. Euroland monetary and economic trends are sensitive to changes in longer-term yields – third chart.

A country breakdown is available for the deposit component of narrow money. Growth is solid across the big four but has cooled recently in Spain while strengthening in Italy – fourth chart.

While monetary trends are hopeful, the economic outlook remains at risk from hostile external policies – a no-deal Brexit and / or US imposition of auto tariffs.

Industrial output has fallen by more in Germany than other Euroland economies, partly reflecting greater sensitivity to Chinese / global trends, but a bounce-back could be imminent. Recent woes were signalled by the six-month change in real M1 deposits of non-financial corporations turning negative in late 2018 but the latter weakness has now reversed – fifth chart.

The August Ifo manufacturing survey, meanwhile, contained glimmers of hope, with the orders inflow balance improving and the finished goods stocks balance consistent with a bottom in the inventory cycle – sixth chart.

Global economic weakness due to monetary policy not trade wars

The preferred narrative of central bankers and mainstream economists is that current global economic weakness primarily reflects US-driven trade policy conflict, which has depressed business confidence and derailed expansion plans. This narrative is false.

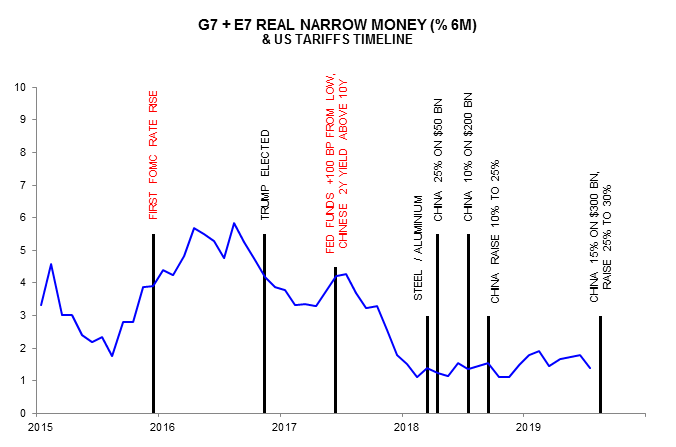

The loss of economic momentum started in H1 2018 and followed a collapse in global six-month real narrow money expansion during H2 2017. This collapse was caused by Chinese and US monetary policy tightening: the Fed had raised rates by 100 bp by June 2017, while the PBoC’s liquidity squeeze on shadow banking had inverted the Chinese government yield curve (i.e. 10-year versus 2-year).

The Trump administration began to impose tariffs only after the monetary shock, with the increase in coverage from $50 billion to $250 billion of Chinese imports proposed in H2 2018, by which time the global economy was already slowing sharply – see chart.

The trade conflict may have contributed to monetary weakness more recently, by suppressing spending plans and associated money demand. A more likely explanation, however, for money growth remaining low is the lagged impact of the further – and excessive – rise in US rates during H2 2017 and 2018.

Other central banks followed the Fed’s mistake of raising rates into monetary weakness, with the UK MPC an egregious offender.

The trade conflict provides a convenient excuse for such actors, enabling them to deflect blame for their policy errors. Mainstream economists are in collusion because of their own failure to forecast economic weakness.

Monetary policies are now easing but moves to date may be insufficient to offset previous excessive tightening and negative trade policy effects. This is suggested by weak July money numbers: as previously discussed, global real narrow money growth appears to have fallen sharply – additional July data this week will provide clarification.