Entries from May 26, 2019 - June 1, 2019

UK corporate money trends flashing red

Simon Ward

Simon Ward

Post a Comment

Post a Comment

A previous post noted that UK corporate narrow money trends were giving a recession warning. The signal has strengthened in April data released today, with the six-month change in real M1 holdings of private non-financial corporations (PNFCs) moving deeper into negative territory – see first chart.

Corporate money weakness is consistent with a squeeze on finances and suggests a faster decline in investment along with job cuts – now being signalled by vacancies data.

The six-month change reached similar levels in 2010-11, following which GDP slowed but did not contract. The global economic backdrop, however, is weaker now, while the negative impact of Brexit uncertainty may not be fully captured in the money numbers.

GDP, moreover, was still far below potential in 2010-11 – recessions usually occur only after the “output gap” has closed.

As previously explained, household narrow money resilience offers little reassurance, as it appears to reflect a portfolio switch out of mutual funds. A broad household savings aggregate encompassing M4 holdings, National Savings and mutual funds ("M4++") has barely grown in real terms over the last six months, suggesting a consumer spending slowdown – second chart.

Labour market watch: job openings rolling over

Last week’s flash PMIs for May confirmed that economic weakness has spread to the US, and from manufacturing to services. The next stage of the downswing, according to the analysis here, will be a crumbling of labour market resilience, which – together with slowing inflation – will add to pressure for central bank policy easing. This is the first of a series of short posts focusing on incoming labour market news.

A previous post noted that UK vacancies (three-month moving average) fell for a third consecutive month in April, signalling a likely decline in employee numbers. The first chart shows that measures of job openings / vacancies rose across economies into early 2018 but are now flatlining or falling across the board.

A drop in German vacancies in May was accompanied by a surprise rise in unemployment – even after adjusting for a reporting change. German aggregate hours worked, meanwhile, fell in the first quarter – second chart.

Euroland money trends suggesting relative resilience

Euroland money growth was little changed in April and continues to give a hopeful message for economic prospects. Global weakness and a reversal of UK pre-Brexit stockbuilding, however, may delay a recovery in momentum until late 2019 / 2020.

Six-month growth rates of real narrow and broad money, as measured by non-financial M1 / M3, edged lower in April but remain well above lows reached in July and March 2018 respectively. The rise from those lows has already been reflected in a small revival in two-quarter GDP momentum – see first chart.

Euroland real narrow money growth, unusually for recent years, is above levels in both the US and China.

In addition, the Kitchin inventory cycle downswing may be further advanced in Euroland relative to other regions. In Germany, in particular, inventories subtracted 0.3 percentage points (pp) from the quarterly change in GDP in the first quarter, following a 0.5 pp drag in the fourth quarter. US inventories, by contrast, contributed positively to GDP growth in the latest three quarters, by a cumulative 0.8 pp.

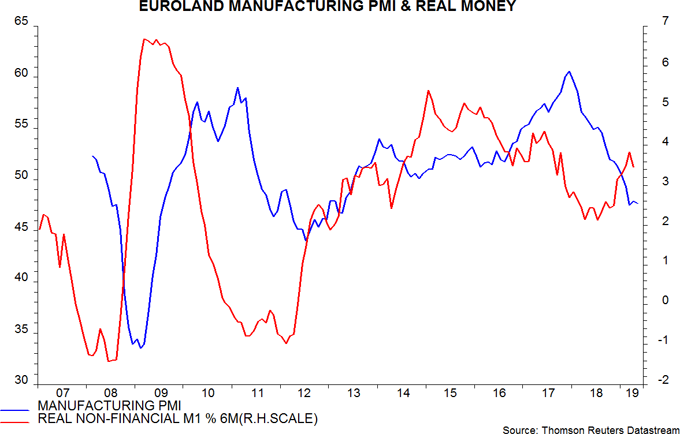

The recovery in real money growth suggests that the manufacturing PMI is at or close to a bottom – second chart.

The main reason for caution is the likelihood of further US / Chinese economic weakness depressing exports and, by extension, business investment. Exports, moreover, have been supported by UK Brexit-related stockpiling, which is now reversing.

Current conditions may be the mirror-image of those in 2016-17. Real narrow money growth moderated over this period but US / Chinese economic strength boosted exports / investment and delayed a peak in the manufacturing PMI until December 2017. Global weakness may now postpone a Euroland economic recovery until 2020.