Entries from August 18, 2019 - August 24, 2019

August PMIs: US / Euroland convergence

Simon Ward

Simon Ward

Post a Comment

Post a Comment

Narrow money trends have been signalling US economic weakness but a stabilisation of momentum in Euroland, with no recession – see, for example, here. August flash PMI results are consistent with this scenario.

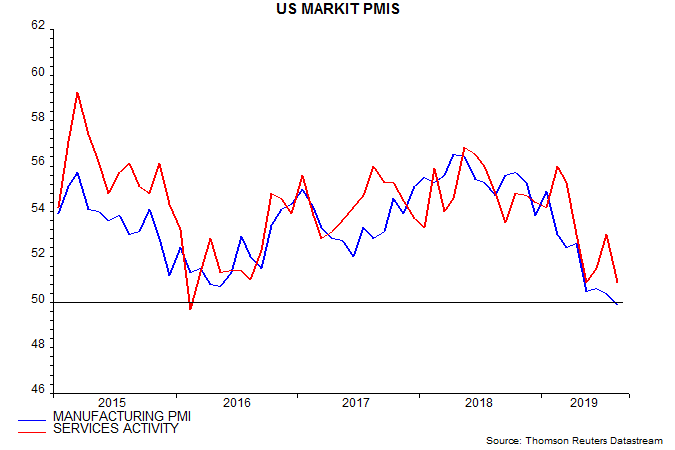

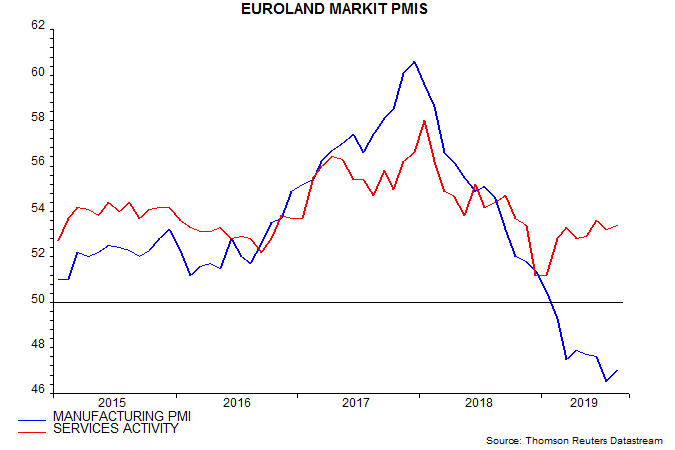

The US composite output index fell sharply in August, returning to its May low. The Euroland index bottomed in January and edged higher in August, moving back above the US level – see first chart.

The US output fall was driven by services activity but the manufacturing PMI slipped below 50, with the new orders component at a 10-year low – second chart.

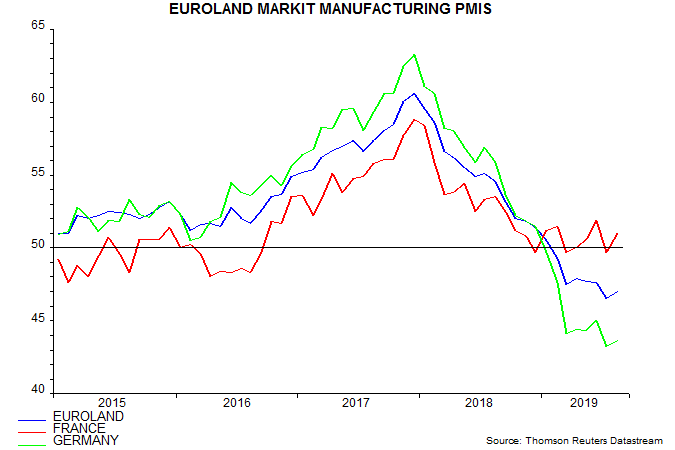

The Euroland manufacturing PMI remains much weaker but edged up in August; services activity, meanwhile, is stronger than in the US – third chart. Manufacturing woes continue to be focused on Germany, reflecting the economy’s sensitivity to negative trends in the auto sector, global capex and China. The French manufacturing PMI is the strongest among the G7 – fourth chart.

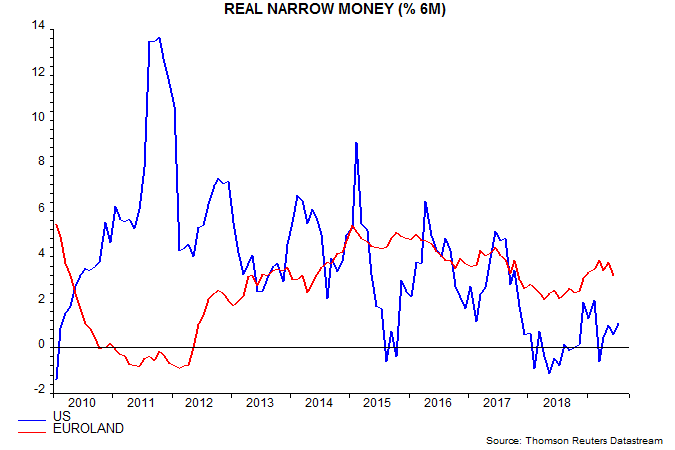

US six-month real narrow money growth edged up in July but remains well below the latest Euroland reading, for June – fifth chart. Euroland growth, however, has cooled recently and a further decline in July data released next week would question the scenario of economic stabilisation.

Why the US yield curve recession signal could prove misleading

Investors were spooked last week by a further inversion of the US Treasury yield curve but the manner of the inversion casts doubt on the validity of the associated recession warning.

Monetary trends are judged here to be a better guide to economic prospects than yield curve movements but the US curve has an impressive record of predicting recessions since the mid 1950s.

The headline development last week was a fall in the 10-year Treasury yield below the 2-year yield, although the cross-over subsequently reversed.

The 10-year / 2-year spread is the favoured curve measure of many market analysts but the 10-year / 1-year spread has a slightly superior historical forecasting record. The latter turned negative ahead of all 9 recessions since the mid 1950s, with only one false signal, in 1965-67 – see first chart. The 10-year / 2-year spread gave an additional false signal in 1998.

Source: Federal Reserve, NBER

The 10-year / 1-year spread turned negative in early August (it had done so briefly in March and May) and the inversion has persisted.

The recent inversion, however, is unusual because it has been driven solely by a decline in longer-term yields.

The second chart separates the 10-year / 1-year spread data according to whether the 1-year yield was higher (red) or lower (green) than 3 months before. All previous inversions, including the false signal in 1965-67, involved a rise in the 1-year yield in addition to or instead of a fall in the 10-year yield.

Source: Federal Reserve, NBER

This distinction suggests a higher risk that the current signal will prove to be false, unless the 1-year yield rises and the curve remains inverted.

Narrow money trends, while continuing to signal weak economic prospects, are not obviously recessionary. The third chart shows the behaviour of real (i.e. CPI-deflated) narrow money before and after the start of the last 9 recessions (red lines) and the 1966-67 slowdown associated with the false yield curve signal (green line). Real narrow money contracted in the 12 months preceding the recession / slowdown start dates but has risen over the past 12 months (blue line).

Source: Federal Reserve, BLS, NBER

Global money trends still downbeat

Incoming narrow money data for July have been disappointing, suggesting that a global economic recovery will be delayed until Q2 2020.

The US, China, Japan, India and Brazil have released July monetary data, together accounting for two-thirds of the global (i.e. G7 plus E7) aggregate tracked here. Incorporating near-complete CPI data, six-month growth of global real narrow money is estimated to have fallen from 1.8% in June to 1.4%, the weakest since March – see first chart.

The July estimate is only slightly above a low of 1.1% reached in October / November 2018. Allowing for an average nine-month lead, the suggestion is that global six-month industrial output momentum will bottom in the current quarter but then bounce around at a weak level through April 2020.

The July reading is far below the 3% level judged here to be necessary to signal an economic recovery, in the sense of a return to trend growth or higher.

The July setback reflected a sharp fall in Chinese real narrow money growth, discussed in a post last week – second chart. Japanese and Brazilian readings were also softer, while US real money growth edged up but remains weak. The July outturn will depend importantly on Euroland and UK data released on 28 / 29 August.