Entries from January 8, 2012 - January 14, 2012

China hard landing risk recedes as real money picks up

Simon Ward

Simon Ward

Post a Comment

Post a Comment

The previous post expressed the hope that a pick-up in emerging E7 real money supply growth would help to compensate for a likely US slowdown, thereby sustaining an expansionary global monetary backdrop. Chinese monetary data for December offer support for this scenario.

Posts here last year drew attention a sharp slowdown in Chinese real money and loan growth, suggesting an increasing risk of a “hard landing”. Policy-makers, however, appear to have averted the danger by easing off on the brakes last autumn, with a consequent revival in nominal monetary trends magnified in real terms by falling inflation.

Six-month real M2 growth in December was the highest since March 2010 (based on seasonally adjusted numbers calculated within Datastream). Real M1 expansion – emphasised by the forecasting approach employed here – has risen by less but, in China’s case, seems to lag real M2, suggesting further improvement in early 2012.

OECD leading indices confirm global lift, real money hints at spring growth peak

The OECD’s leading indices continued to recover at the margin in November, confirming an earlier signal of global economic improvement from real money supply trends.

The chart shows six-month growth rates of G7 plus emerging E7 industrial output and real narrow money together with a composite leading indicator derived from the OECD indices. Real money typically moves about six months ahead of output while the indicator leads by about three months.

The indicator was very weak last summer but moved back into positive territory in October and rose further in November, reaching its highest level since February. This suggests that the late 2011 recovery in global industrial momentum will be sustained in early 2012.

Six-month real money expansion, however, appears to have peaked in October, consistent with output growth topping out in the spring. Such a scenario would be confirmed by a peak in the OECD-based indicator in early 2012, probably January.

The view here of economic prospects for later in 2012 will be conditioned by the extent of any further real money slowdown. The hope is that a likely weakening of US monetary trends will be counterbalanced by a pick-up in the E7 and Euroland in response to recent and prospective policy easing.

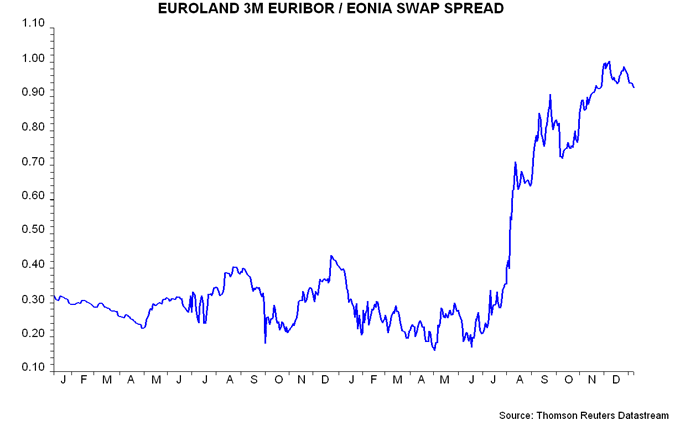

Are Eurozone banks "hoarding" liquidity?

Media reports continue to refer to the level of balances in the ECB’s deposit facility as a gauge of liquidity “hoarding” by banks. If only it were so simple.

An increase in the ECB’s lending to banks in repo operations automatically injects liquidity into the system. Banks hold this cash either in their current accounts at the ECB or the deposit facility. Since they earn no interest on current account balances in excess of reserve requirements, it mostly ends up in the deposit facility.

Suppose that banks with more cash increase lending or buy existing securities (i.e. they don't "hoard"). The cash is transferred to other banks (those where the recipients of the lent funds or the sellers of the securities hold their accounts), whose current account / deposit facility balances therefore rise. The aggregate position falls only if the cash flows to weaker banks, who repay lending from the ECB, thereby withdrawing liquidity from the system. Otherwise, use of the deposit facility will remain high even though banks are not “hoarding”. (Liquidity can also be withdrawn by banks buying new government securities, resulting in cash being transferred from banks’ to governments’ accounts with the ECB.)

The daily deposit facility numbers, therefore, provide little information about banking system activity and risk aversion – the latter is better captured by the three-month Euribor / overnight interest rate swap spread, which yesterday fell to its lowest level since late November.