Entries from December 1, 2023 - December 31, 2023

UK inflation: "monetarist" forecast on track

Simon Ward

Simon Ward

1 Comment

1 Comment

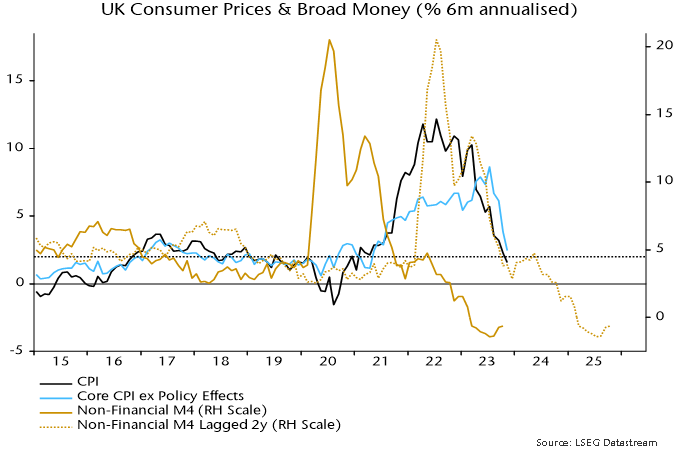

The MPC’s November inflation projections are ancient history. Price pressures have plunged in line with a simplistic monetarist forecast suggesting a return to target in Q2 2024 and an undershoot in H2.

The simplistic forecast is based on the Friedmanite rule that inflation directionally follows money growth with an average lag of two years. This is converted to a numerical profile by assuming a one-for-one relationship of deviations in inflation and money growth from 2% and 4.5% respectively.

Friedman emphasised the variability of the money growth / inflation lag but a two-year assumption has proved accurate in timing the inflation peak and subsequent decline – see chart 1.

Chart 1

A post in July suggested that the six-month rate of increase in the CPI, seasonally adjusted, would fall to 2% annualised or lower around end-2023, reflecting a decline in six-month broad money growth to below 4.5% annualised in Q4 2021. The fall is ahead of schedule, with the six-month CPI increase at 1.6% in November.

The simplistic forecast suggests that six-month inflation will fluctuate around the current level through mid-2024 before dropping further in H2 – chart 1. The implication is that the annual rate will return to target in Q2 and undershoot during H2.

By contrast, the modal forecast for annual inflation in Q4 2024 in the November Monetary Policy Report was 3.1%, with the mean forecast (incorporating an upside risk assessment) at 3.4%.

Broad money momentum remains negative, suggesting that an inflation revival is unlikely before mid-2025.

Bottom-up considerations support the view that annual inflation will return to target by next spring, assuming no adverse shocks:

-

Annual inflation of food, alcohol and tobacco of 9.4% in November could fall to 3% by Q2. Annual producer output price inflation of food, beverages and tobacco is already down to 2.1%, while input prices of home-produced food are falling year-on-year.

-

The energy price cap will rise by 5% in January but Cornwall Insight currently projects a 14% cut in April.

-

Annual core goods inflation of 3.3% in November could fall to 1%. Core producer output prices are flatlining, while base effects are favourable through May.

-

Slowing food prices will feed through to catering services, with the historical sensitivity suggesting a fall in annual inflation from 7.8% in November to 4.5%. This would cut services inflation by 0.75 pp, based on the 23% weight of catering in the services basket.

-

The above two assumptions coupled with a 1 pp slowdown in the rest of the services basket would imply a 1.75 pp fall in annual core inflation by Q2 (5.1% in November). This would be sufficient to generate a 2% headline rate given the assumed food slowdown and a large year-on-year decline household energy bills.

US business money diverging positively from weak Europe

Recent US / European monetary weakness gives a negative signal for economic prospects through mid-2024, at least. US trends, however, are showing signs of improvement in aggregate and in terms of sectoral developments, suggesting smaller downside risk and earlier recovery prospects.

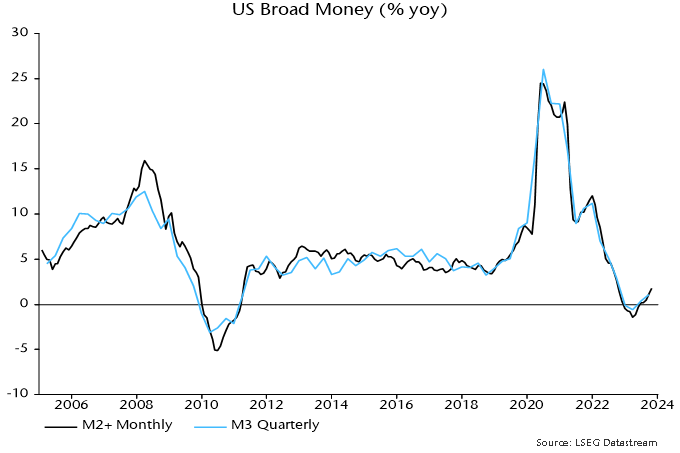

The monthly measure of US broad money tracked here adds commercial bank large time deposits and institutional money funds to the Fed’s M2 aggregate (“M2+”). The former items are important for capturing corporate and institutional money holdings.

The monthly aggregate can be cross-checked against a quarterly M3 measure derived from the Fed’s financial accounts, which additionally includes repurchase agreements. Annual rates of change of the two measures bottomed in March and have recovered to weak positive territory (1.8% for M2+ in October, 1.1% for M3 in September) – see chart 1.

Chart 1

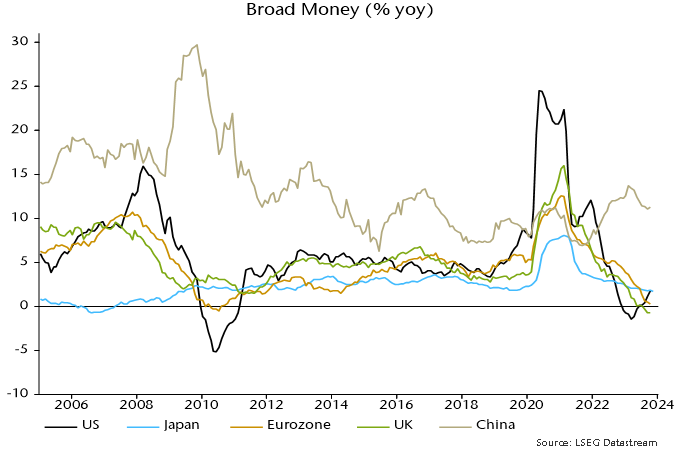

This recovery contrasts with a further decline in annual rates of change of Eurozone and UK broad money, as measured by non-financial M3 and non-financial M4 respectively. The UK series crossed below the US level in July, with the Eurozone following in September – chart 2.

Chart 2

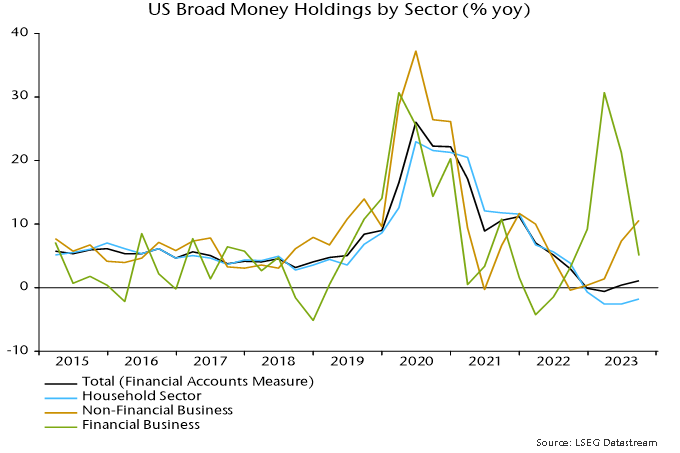

The suggestion that US economic prospects for later in 2024 are less bad than in Europe and improving at the margin is supported by sectoral money developments. Aggregate money is the best guide to economic prospects but changes in business / corporate liquidity usually carry more significance than fluctuations in household money holdings, reflecting their influence on decisions about investment and hiring.

The sectoral M3 breakdown in the Fed’s financial accounts shows that still-weak aggregate broad money growth is explained by a continued fall in the household component, while money holdings of non-financial businesses have bounced back, rising by 10.6% in the year to September – chart 3*.

Chart 3

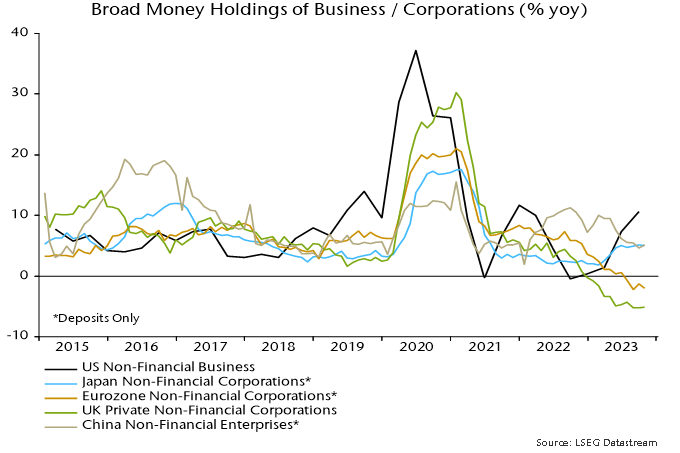

By contrast, annual rates of change of money holdings of Eurozone / UK non-financial corporations remain negative, with no sign of recovery – chart 4.

Chart 4

The pick-up in US business money holdings is surprising and may not be sustained but current US / European monetary divergence suggests that US economic outperformance will continue, while a reversal of policy tightening is more urgently required in the Eurozone / UK.

*The pick-up in business money is not fully captured by M2 (because much of the inflow has been into large time deposits and institutional money funds), explaining why M2 is lagging M2+ / M3, falling by 3.3% in the year to October (versus 1.8% growth of M2+).

Questioning US economic "strength"

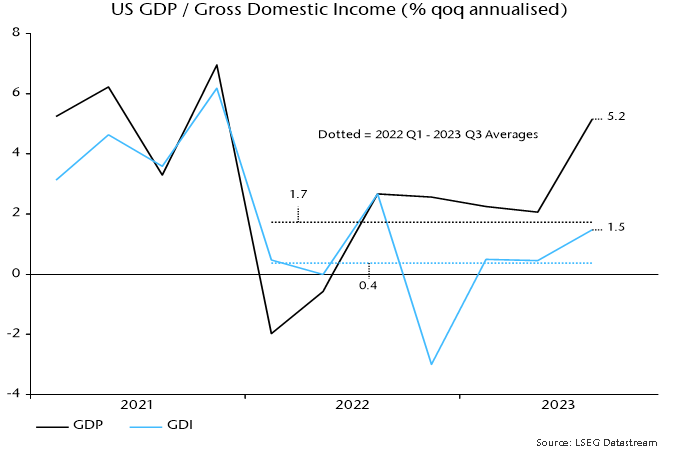

The 5.2% annualised increase in the headline expenditure-based measure of US GDP in Q3 partly represents payback for earlier weakness. GDP has risen at a modest 1.7% annualised pace since end-2021, well below average expansion of 2.5% in the five years preceding the pandemic (i.e. to end-2019).

The alternative income-based measure of GDP – gross domestic income – paints a much more miserable picture. GDI grew by 1.7% annualised in Q3 alone and by only 0.4% in the seven quarters since end-2021 – see chart 1.

Chart 1

It has been suggested that the GDP / GDI divergence is capturing an increased reliance on borrowing and / or savings depletion to finance spending. This is incorrect: GDP and GDI measure the same concept and the divergence reflects a rising statistical discrepancy, with GDP 2.6% higher than GDI in Q3.

The higher level of GDP does not imply that the GDI measure is less inclusive or accurate. Research by Jeremy Nalewaik, then a Fed economist, found that early GDI estimates were a better gauge of cyclical fluctuations and predicted the direction of future revisions to GDP.

If the national accounts evidence suggests lacklustre performance at best, what explains the consensus perception of US economic “strength”?

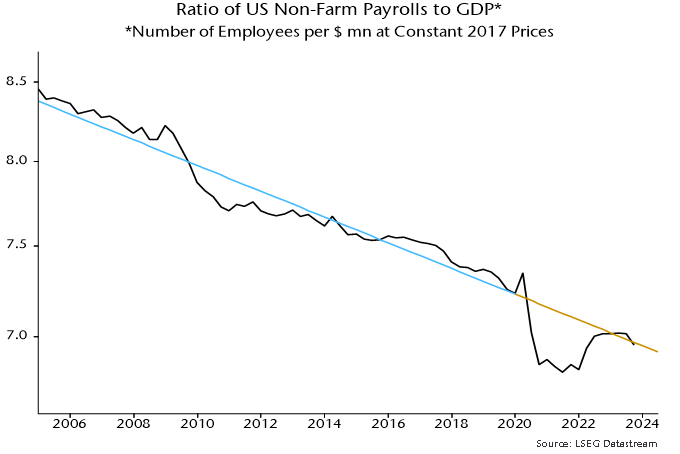

The answer seems to be unusually rapid growth of payroll employment. Payrolls rose at a 2.8% annualised rate between Q4 2021 and Q3, significantly outpacing GDP expansion of 1.7%.

Payrolls strength is judged here to reflect a normalisation of the relationship with the level of GDP, following an undershoot of trend during the pandemic – chart 2. This adjustment appears complete, implying that payrolls will lag GDP going forward (the slope of the trend line implies an annualised growth shortfall of 1.0%).

Chart 2

The GDP / GDI contrast is particularly stark over the latest four quarters, during which GDP grew by 3.0% but GDI contracted by 0.2%.

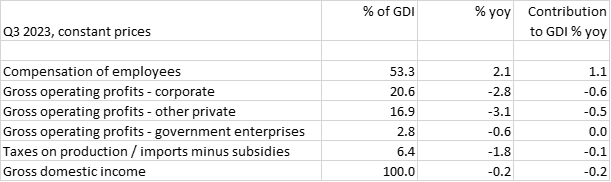

The table below shows the contributions of GDI components to its change over the past year. With real wage income growing solidly, GDI contraction was attributable to falls in real operating profits of corporations and other private enterprises.

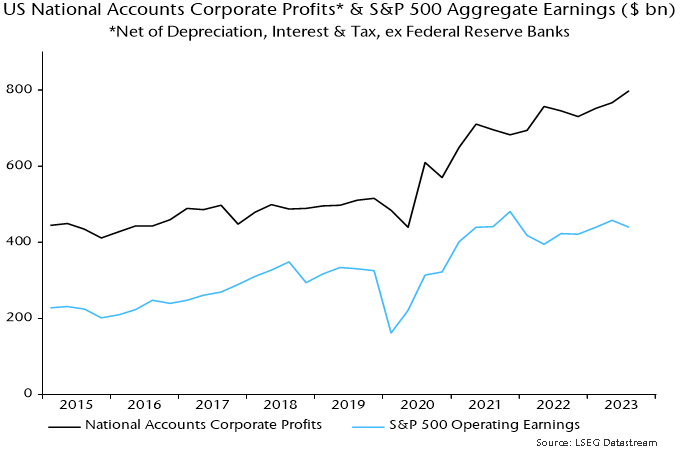

Is national accounts profits weakness consistent with company earnings data? GDI operating profits are gross of depreciation, interest and taxes and exclude foreign earnings, so adjustments are necessary to align with S&P 500 earnings. Chart 3 compares nominal data for S&P 500 aggregate operating earnings and an equivalent national accounts-based measure for corporations excluding the Fed. S&P earnings grew more slowly in the year to Q3, so there is no suggestion of a negative discrepancy in the national accounts numbers.

Chart 3

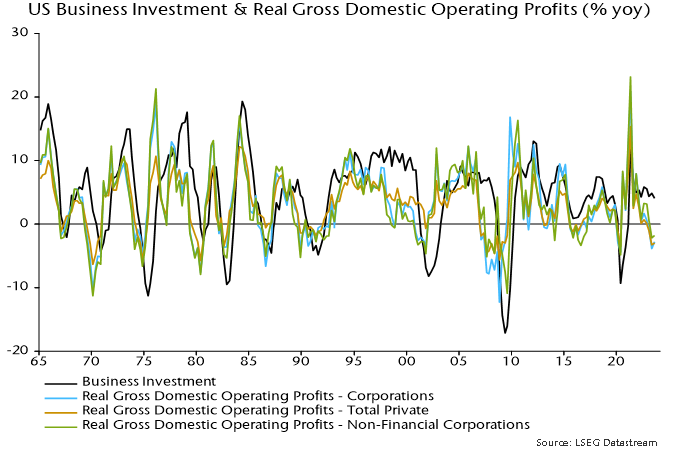

Real operating profits are a leading indicator of business investment so the contraction in recent quarters suggests a capex downturn ahead – chart 4.

Chart 4